WinSavvy Editorial Standards

How this article was created

Insurance is one of the hardest products to market because people rarely wake up excited to buy it. They know they need protection, but they often delay the decision until a big life event, a legal need, a loan process, a business risk, or a painful reminder pushes them to act. That is why marketing insurance is not just about getting more clicks. It is about building trust before the buyer is ready, making the product easy to understand, and helping people feel safe enough to take the next step.

Build the strategy around trust before you build it around traffic

Insurance marketing starts with one hard truth. People do not buy insurance only because they saw an ad. They buy because they believe the company understands their risk, explains the product clearly, and will stand by them when something goes wrong.

That means trust has to come before traffic. If your campaign brings visitors but your message feels cold, confusing, or too sales-heavy, people will leave. They may not say no to insurance. They may say no to you.

Your first job is to lower doubt

A person looking for insurance usually has many quiet questions in their mind. They wonder if they are paying too much. They wonder if they are buying too little cover. They wonder if the agent is pushing the plan that pays the highest commission. They wonder if the claim process will be painful later.

Good marketing answers these doubts before they become objections.

Your website, ads, emails, and sales pages should make people feel that they are in safe hands. This does not mean using big promises. In fact, big promises can hurt trust in insurance. Simple, clear, honest language works better.

Use plain language to make risk feel manageable

Most insurance pages lose buyers because they sound like policy documents. They use terms people do not use in daily life. They explain features before explaining why those features matter. They assume the buyer already understands the product.

A better way is to write like a helpful advisor sitting across the table.

For example, instead of saying, “Our policy offers comprehensive protection against covered perils subject to exclusions,” say, “This plan helps protect you from major losses listed in your policy, such as fire, theft, or certain types of damage. We will also show you what is not covered, so there are no surprises later.”

That small shift matters. It makes the product feel less scary. It also makes your brand feel more honest.

Trust should show up on every page

Many insurance brands place trust signals only on their home page. They add a few reviews, badges, awards, or partner logos, then assume the job is done. But buyers may enter your site from a blog post, a quote page, a local landing page, or a paid ad.

Every important page should help the visitor feel safe.

This can be done through customer stories, clear explanations, visible contact details, simple disclaimers, helpful FAQs, claim support details, and proof that real people are behind the brand. If you serve a local market, show your local presence. If you serve a specific industry, show that you understand that industry’s risks.

Make the buyer feel guided, not hunted

Insurance buyers do not want to feel chased. They want to feel helped. So your calls to action should match where the person is in their journey.

Someone reading “What does renters insurance cover?” may not be ready to request a quote right away. They may first need a simple guide or a coverage checklist. Someone searching “best car insurance for new drivers in Dallas” may be closer to comparing options.

Someone searching your brand name plus “reviews” may need proof and reassurance.

This is where many campaigns fail. They push the same action to every visitor. A better strategy is to offer the next natural step. Invite early-stage readers to learn more. Invite comparison-stage visitors to get a quote. Invite high-intent visitors to speak with an advisor.

When the action feels natural, conversion feels easier.

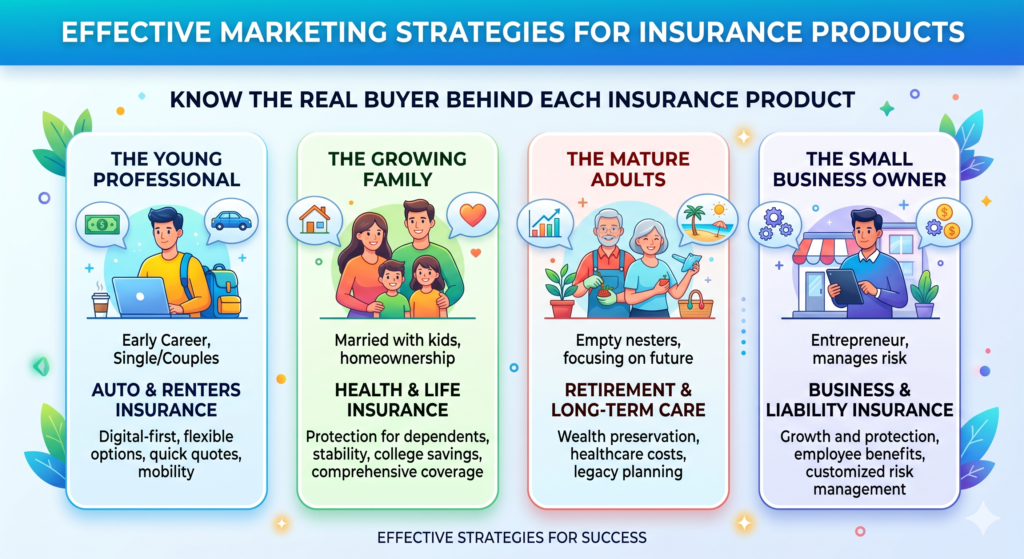

Know the real buyer behind each insurance product

Every insurance product has a different emotional trigger. Life insurance is often tied to family and responsibility. Health insurance is tied to safety and access to care. Auto insurance is tied to legal need, cost, and peace of mind. Business insurance is tied to risk, survival, and protecting what someone has built.

If you market all these products with the same message, your campaigns will feel flat. The product may be insurance, but the buyer’s fear, hope, urgency, and decision process are different each time.

Start with the reason people buy, not the product you sell

A common mistake in insurance marketing is starting with policy features. Brands talk about coverage limits, add-ons, premiums, riders, exclusions, and claim terms. These things matter, but they are not always the first thing buyers care about.

People first want to know, “Is this right for me?”

A young parent thinking about life insurance is not really buying a policy. They are buying the feeling that their family will not be left helpless. A small business owner buying liability insurance is not just buying cover. They are buying the ability to keep working even if something goes wrong.

Map each product to the buyer’s daily worry

Your marketing becomes stronger when it connects the product to a real-life worry.

For home insurance, the worry may be, “What happens if my house is damaged and I cannot afford repairs?” For travel insurance, the worry may be, “What if my trip is cancelled or I get sick abroad?” For cyber insurance, the worry may be, “What if my business gets attacked and I lose client trust?”

Once you know the daily worry, your message becomes sharper. You can write better ads, better landing pages, better emails, and better blog posts. You can also remove weak claims that do not move the buyer.

Instead of saying, “Protect what matters most,” which is too broad, you can say, “Keep your business running even if one accident leads to a costly claim.” That is clearer. It speaks to a real fear. It also tells the buyer why the product matters now.

Segment buyers by life stage and risk stage

Insurance buyers are not only different by age, income, or location. They are also different by life stage and risk stage.

A person buying their first car has different needs from a parent adding a teen driver. A newly married couple has different life insurance questions from a couple with two children and a mortgage. A startup with five employees has different business insurance needs from a company entering a new market.

This is why broad campaigns waste money. They speak to everyone, so they connect with no one.

Create message paths for each buyer group

A strong insurance marketing strategy should have separate message paths for different buyer groups. These paths do not have to be complicated. They simply need to match what the buyer cares about.

For first-time buyers, focus on education and clarity. Explain what the product does, what affects price, and how to avoid common mistakes. For switchers, focus on savings, better service, claim support, and easier policy management. For high-risk or complex buyers, focus on expert guidance, tailored cover, and confidence.

This approach helps your content feel personal without needing to be overly fancy. It also helps your sales team because leads arrive with clearer intent.

When buyers feel that your message was written for their situation, they stay longer, trust more, and move faster.

Turn SEO into a lead engine, not just a traffic source

SEO can be one of the strongest channels for insurance products because people search when they have real questions. They search when they are confused, comparing, worried, or ready to buy. But not all insurance SEO is useful.

Many agencies chase high-volume keywords and end up attracting people who are not ready, not qualified, or not in the right market. Better insurance SEO is built around intent. It asks, “What does this person need right now, and what should they do next?”

Build content around buyer intent

There are usually three major search stages in insurance. The first is learning. The buyer wants to understand a product. The second is comparing. The buyer wants to know which option is better. The third is acting. The buyer wants a quote, agent, provider, or policy.

Each stage needs different content.

A learning keyword might be “what does business liability insurance cover.” A comparison keyword might be “general liability vs professional liability insurance.” An action keyword might be “small business insurance broker near me.”

If you treat all three the same, you will lose conversions. A learning page should explain clearly. A comparison page should help the buyer choose. An action page should make it easy to contact you or request a quote.

Match every page to one clear next step

Every SEO page should have a job. Some pages build trust. Some collect leads. Some help buyers compare. Some support sales. Some bring local traffic. The mistake is expecting every page to sell directly.

For example, a blog post explaining “how much life insurance do I need” should not sound like a hard sales pitch from the first paragraph. It should teach first. Then it can invite the reader to use a calculator, download a guide, or speak with an advisor.

A local service page for “home insurance agent in Phoenix” can be more direct. That visitor is likely closer to action. The page should show location relevance, service details, trust proof, and a quote option.

This is how SEO becomes a lead engine. You stop writing random posts. You build a path from question to trust to action.

Focus on long-tail keywords with buying signals

Insurance keywords can be very competitive. Broad terms like “life insurance” or “car insurance” are hard to rank for and often expensive in paid search. Long-tail keywords are usually better because they show clearer need.

A person searching “best health insurance for self-employed parents” is telling you much more than a person searching “health insurance.” A business owner searching “does a cleaning company need liability insurance” has a clear problem. These searches may have lower volume, but they often bring better leads.

Use simple content clusters for each product

A content cluster is a group of related pages that support one main topic. For insurance SEO, this works very well because each product has many related questions.

For example, if you sell commercial insurance, you can build a main page about business insurance and support it with detailed pages on liability insurance, property insurance, workers’ compensation, professional liability, industry-specific cover, cost guides, claim questions, and local service pages.

The goal is not to publish more for the sake of publishing. The goal is to cover the buyer’s real decision journey better than your competitors.

When your website answers more useful questions, search engines can understand your expertise more clearly. More importantly, buyers feel they can trust you because you have helped them before asking for their details.

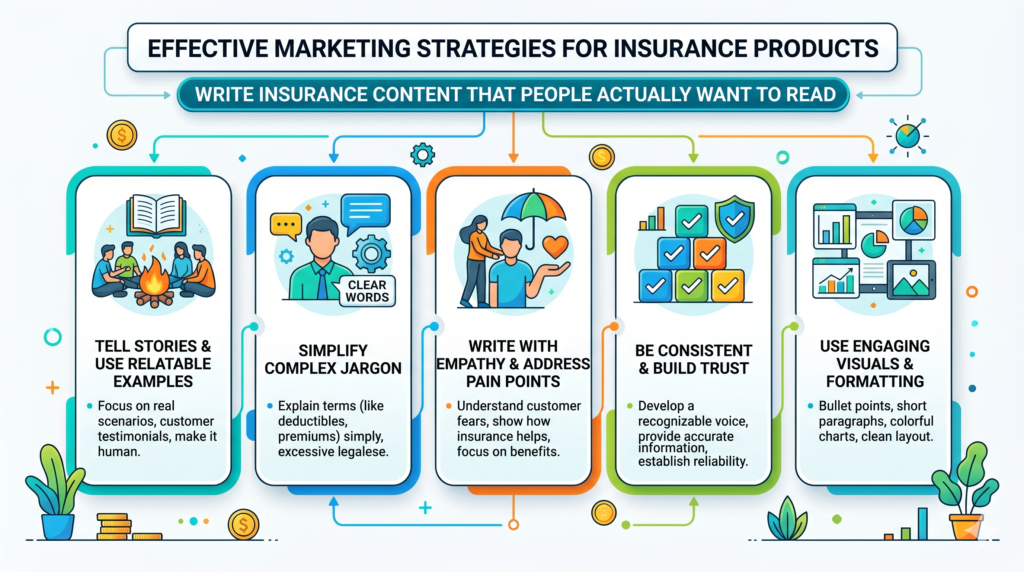

Write insurance content that people actually want to read

Insurance content is often boring because it is written for approval, not for people. It sounds safe, but it does not help. It uses long sentences, stiff wording, and generic advice. It tells people what they already know, then ends with a weak call to action.

Good insurance content should feel like guidance. It should make the reader smarter, calmer, and more ready to act.

Open with the buyer’s problem

The first few lines of any insurance article, landing page, or email should show that you understand the reader’s situation. Do not begin with a company history. Do not begin with a broad statement like, “Insurance is important in today’s world.” People already know that.

Start with the problem.

For example, if you are writing about renters insurance, begin with the fear that many renters think the landlord’s policy protects their belongings, only to find out later that it does not. If you are writing about business insurance, begin with the risk of one accident, client dispute, or property loss creating a bill the business cannot easily handle.

Make the reader feel seen before you teach

People pay more attention when they feel understood. This is a copywriting rule that matters deeply in insurance.

Before explaining policy details, reflect the buyer’s concern in plain words. Say what they are likely thinking. Say what mistake they may be trying to avoid. Say why the choice feels confusing.

Then teach.

This order works because it lowers resistance. The reader does not feel like they are being lectured. They feel like someone is finally explaining the topic in a way that makes sense.

Explain value before explaining features

A feature is what the policy includes. Value is why that feature matters.

Many insurance pages list features too early. They say things like coverage amount, deductible options, add-on cover, roadside help, claim support, or policy flexibility. These are useful, but they need context.

A buyer wants to know how each feature protects them in real life.

Turn every feature into a real-world outcome

If a policy has roadside assistance, explain that it can help when the car breaks down late at night or during a family trip. If a business policy includes professional liability, explain that it can help if a client claims your work caused them financial loss.

If health insurance includes a wide hospital network, explain that it gives the family more care options when they need treatment.

This makes the product easier to understand. It also makes the value feel real.

Insurance buyers do not always remember every feature. But they remember the moment when they understood why the feature matters.

Keep the writing simple without making it shallow

Simple writing does not mean weak writing. It means the reader does not have to fight to understand you.

Use short sentences when the idea is important. Use examples when the topic is complex. Explain one idea at a time. Avoid legal-heavy language unless it is required, and when it is required, explain it in plain words nearby.

Sound like a human advisor, not a brochure

The best insurance content sounds calm, clear, and useful. It does not overhype. It does not scare people too much. It does not hide the hard parts.

For example, when talking about price, be honest that the final premium depends on several factors. Then explain those factors simply. When talking about claims, avoid making promises you cannot keep. Instead, explain the process, the documents needed, and how your team helps.

This builds more trust than polished slogans.

Strong content is not about sounding clever. It is about making the buyer feel, “Now I understand what to do.”

Build landing pages that make the quote request feel easy

A landing page for an insurance product has one main job. It must help the visitor feel confident enough to take the next step. That step may be requesting a quote, booking a call, starting an application, or comparing options.

The mistake many insurance brands make is treating a landing page like a digital brochure. They add a product summary, a form, and a few generic lines about protection. Then they wonder why visitors do not convert. The problem is not always traffic quality. Often, the page does not answer enough questions, reduce enough fear, or make the next step feel simple.

The page should match the promise that brought the visitor there

If someone clicked an ad about affordable car insurance for new drivers, the landing page should speak directly to new drivers. If someone searched for small business insurance for contractors, the page should talk about contractor risks, job-site accidents, tools, client claims, and certificates of insurance.

A page that feels too broad creates doubt. The visitor thinks, “Is this really for me?” Once that doubt appears, conversion becomes harder.

Keep the opening clear and specific

The top of the landing page should quickly answer three questions. The visitor should understand what product you offer, who it is for, and why they should keep reading. This should happen without complex words or long claims.

A strong opening for a business insurance page might say that you help small business owners compare cover for accidents, property damage, client claims, and employee-related risks. That is simple. It tells the reader what you do. It also connects the product to real problems.

Do not start with a vague headline like “Protect your future today.” It sounds nice, but it does not explain anything. In insurance, clarity beats cleverness.

The form should feel safe, short, and worth completing

Forms are often where insurance landing pages lose leads. People may want a quote, but they may not want to give too much personal information before they trust you.

This is especially true for products like health insurance, life insurance, business insurance, and high-value home insurance. These forms can feel serious. If the page asks for too much too soon, the visitor may leave.

Explain what happens after the form

A simple note near the form can improve trust. Tell people what will happen after they submit their details. Let them know whether they will get a call, an email, a quote comparison, or a consultation. Tell them how soon they can expect a response if you can do so honestly.

This removes uncertainty.

For example, instead of only saying “Get a quote,” you can say, “Share a few details and our team will help you compare suitable options. We will explain the next steps before you choose anything.”

That sentence makes the action feel less risky. It also makes the lead feel guided instead of sold to.

Use proof where the buyer feels doubt

Social proof should not be placed randomly. It should appear where the visitor may hesitate. If the buyer may doubt your expertise, show reviews or years of experience. If the buyer may worry about claims, explain how support works. If the buyer may worry about cost, explain how you help compare options.

Proof should support the decision, not decorate the page.

Make trust signals specific, not generic

A generic testimonial that says “Great service” is better than nothing, but it does not say much. A stronger testimonial explains what problem the customer had and how your team helped.

For example, a review from a small business owner saying that your team helped them get a certificate of insurance quickly before a contract deadline is more useful than a broad compliment. It shows a real use case. It also speaks to other business owners with the same need.

Landing pages work best when every part has a reason to exist. The headline brings the visitor in. The copy explains the value. The proof lowers doubt. The form feels easy. The call to action feels like the next safe step.

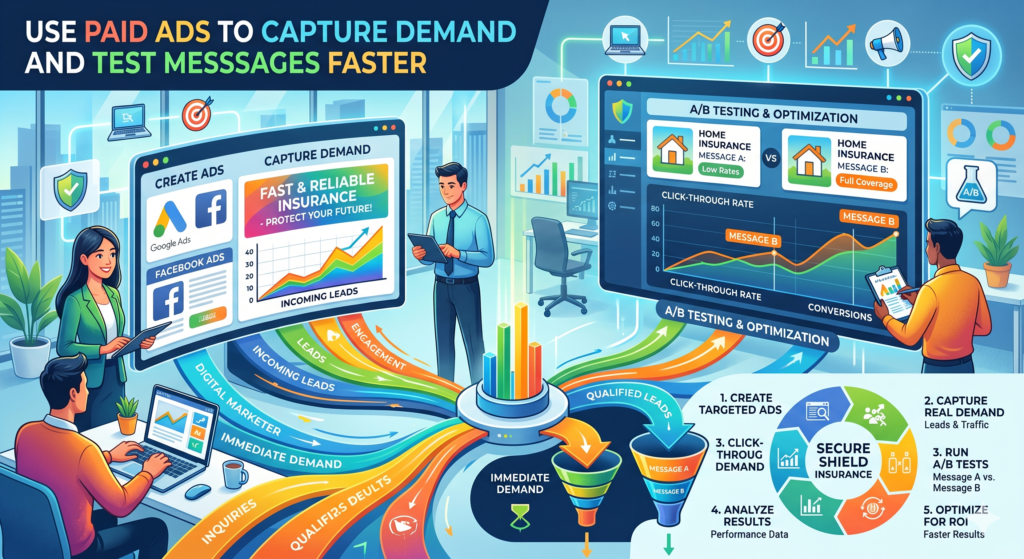

Use paid ads to capture demand and test messages faster

Paid ads can work very well for insurance, but they can also waste money very quickly. Insurance keywords are often expensive because the value of a customer can be high. This means every click matters.

The goal is not just to get traffic. The goal is to learn which message brings the right buyer at the right cost. Paid ads give you faster feedback than SEO. You can test offers, headlines, locations, product angles, and landing pages before investing months into a larger campaign.

Search ads should focus on strong intent

Search ads are powerful because the buyer is already looking for something. A person searching for “business insurance quote for cleaning company” is showing clear intent. A person searching for “what is insurance” is not as close to buying.

This does not mean you should ignore early-stage searches forever. But when budget is limited, start with high-intent terms. These are searches that include words like quote, cost, agent, near me, compare, provider, policy, or a specific insurance type tied to a need.

Do not send every paid click to the same page

One of the fastest ways to waste paid ad budget is sending all traffic to a generic home page. The home page has too many jobs. It talks about the whole brand. It may not match the exact search.

A better approach is to create focused landing pages for each major campaign. If the ad is about commercial auto insurance, send users to a commercial auto page. If the ad is about life insurance for parents, send them to a page that talks to parents.

This improves quality because the visitor sees a message that matches what they searched. It also helps you measure which product pages and buyer groups convert best.

Social ads should create demand, not just chase it

Social media ads work differently from search ads. People are not usually scrolling through Facebook, Instagram, LinkedIn, or YouTube hoping to buy insurance. So the ad needs a different job.

For many insurance products, social ads work best when they educate, warn, remind, or create awareness. They can bring people into your funnel before they search on Google.

Use story-based angles instead of hard selling

A social ad that says “Buy insurance now” may be ignored. But an ad that explains a common mistake may get attention.

For example, a renters insurance ad can start with the fact that many renters think their landlord’s policy protects their personal items, when it usually does not. A business insurance ad can talk about how one client claim can create legal costs even if the business did nothing wrong.

A life insurance ad can talk about how major life events are often the moment people realize they need cover.

These angles work because they meet the buyer where they are. They do not demand action too early. They open a loop in the buyer’s mind and make them want to learn more.

Retargeting should be calm and helpful

Retargeting is important because insurance buyers often do not convert on the first visit. They compare, think, ask family members, speak to partners, and come back later.

But retargeting should not feel pushy. Seeing the same quote ad ten times can make the brand feel desperate. Instead, use retargeting to answer the next question.

Show content based on the page they visited

If someone visited your life insurance page, retarget them with a guide on how much cover a family may need. If someone visited your business insurance page, show them a simple article on common coverage gaps for small businesses. If someone started a quote form but did not finish, invite them back with a message that makes the process feel easy.

Paid ads become stronger when they are part of a journey. The first ad gets attention. The landing page builds trust. The follow-up ad answers doubt. The final call to action helps the buyer act.

That is much better than showing the same “Get a quote today” message to everyone.

Make email marketing feel like advice, not pressure

Email is one of the most useful channels for insurance marketing because buying insurance often takes time. People may download a guide, check a quote, ask a question, or visit a page long before they are ready to buy.

Email helps you stay present during that gap. But it only works when it feels helpful. If every email pushes a sale, people stop reading. If every subject line feels urgent, people stop trusting you.

Start with the buyer’s stage

Not every lead should receive the same email sequence. A person who downloaded a beginner guide needs education. A person who requested a quote needs support and follow-up. A person whose policy is near renewal needs a different message. A past customer needs retention, review, referral, and cross-sell communication.

Good email marketing begins by understanding the person’s stage.

Write the first email to confirm the decision they just made

The first email after a form submission should not feel like a cold sales pitch. It should confirm that the person took the right step. It should explain what they will receive, what they can expect, and how you can help.

For example, if someone downloads a guide about home insurance, the first email can thank them and explain how the guide will help them avoid common gaps. It can also invite them to reply with questions. That small invitation makes the brand feel human.

If someone requests a quote, the first email should be even clearer. Tell them the next step, remind them what information may be needed, and make it easy to contact your team.

Educate before asking for action

Insurance decisions are full of questions. Email gives you a chance to answer those questions over time.

For life insurance, you can explain how cover amount works, why age matters, what affects cost, and how to compare term and permanent options. For business insurance, you can explain common risks, coverage gaps, certificates, claims, and renewal planning.

For auto insurance, you can explain deductibles, driver history, bundling, and ways to lower premiums.

Each email should solve one small problem

A strong email does not try to explain the whole product at once. It focuses on one concern and makes it easier to understand.

One email can explain what a deductible means in plain words. Another can explain why the cheapest policy may not always be the safest choice. Another can show when it makes sense to review coverage.

This keeps the email useful. It also trains the reader to open future emails because they expect clear advice, not noise.

Use email to support renewals and retention

Many insurance marketers focus heavily on new leads and forget existing customers. That is a mistake. Renewal campaigns, policy review emails, claim support messages, and helpful seasonal reminders can protect revenue and increase customer value.

A customer who already trusts you is often easier to retain than a new customer is to win.

Make renewal emails useful before they become urgent

Do not wait until the last minute to talk about renewal. Start early with helpful reminders. Explain what may have changed in the customer’s life or business since the last policy period. Invite them to review coverage before renewal.

For example, a business may have hired staff, bought equipment, signed larger contracts, or moved offices. A family may have bought a new home, had a child, changed jobs, or added a driver. These changes can affect coverage needs.

When renewal emails feel like guidance, customers are more likely to stay. They see that you are not just collecting premiums. You are helping them stay protected.

Use local SEO and community presence to win high-trust buyers

Insurance is often personal. Even when people research online, many still like knowing that a real person or local team can help them. This is why local SEO can be powerful for agents, brokers, and regional insurance companies.

Local marketing works because it blends digital visibility with human trust. When someone searches for an insurance agent near them, they are often ready to act. They want help, not just information.

Your local pages should prove you understand the area

A local insurance page should not be a copied service page with the city name changed. Buyers can feel when a page is thin. Search engines can also struggle to see real value when every location page says the same thing.

A strong local page should explain the products you offer in that area, the type of customers you serve, and the local risks that matter.

Connect insurance needs to local realities

If you sell home insurance in an area with storm risk, talk about storm-related concerns in a careful and clear way. If you sell business insurance in a city with many contractors, restaurants, or professional firms, speak to those business types.

If auto insurance costs are affected by local driving patterns, traffic, or theft concerns, explain the factors without making claims you cannot support.

This makes the page more useful. It also shows that your business is not just targeting the location for SEO. You actually understand the people there.

Reviews can carry more weight than your own claims

For local insurance, reviews are often one of the first trust checks. People want to know whether your team is responsive, clear, helpful, and fair. They also want to see how you handle real situations.

A strong review profile can improve both clicks and conversions. But reviews should be earned honestly and handled carefully.

Ask for reviews after helpful moments

The best time to ask for a review is after a positive service moment. This could be after helping a customer understand a policy, finish a smooth onboarding process, solve a billing question, or receive support during a claim.

Do not ask in a way that pressures the customer. Keep it simple and respectful. Let them share their honest experience.

Also respond to reviews in a human way. Thank people for their feedback. Keep private details out of public replies. If a review raises a concern, respond calmly and invite the person to continue the conversation privately.

Community marketing should support trust, not just visibility

Local insurance brands can build strong trust by being present in the community. This can include local events, small business groups, school programs, homeowner workshops, chamber meetings, and partnerships with related professionals.

But the goal should not be to place your logo everywhere. The goal should be to become known as a helpful local resource.

Teach simple risk lessons in local spaces

A local agency can host short sessions on topics like preparing for storm season, understanding business liability, reviewing insurance after buying a home, or protecting a family with life insurance. These topics do not need to be dramatic. They need to be useful.

When people learn from you before they buy from you, they remember you differently. You are no longer just another insurance provider. You become the person or team who made a confusing subject easier.

That is the real power of local marketing. It turns trust into a market advantage.

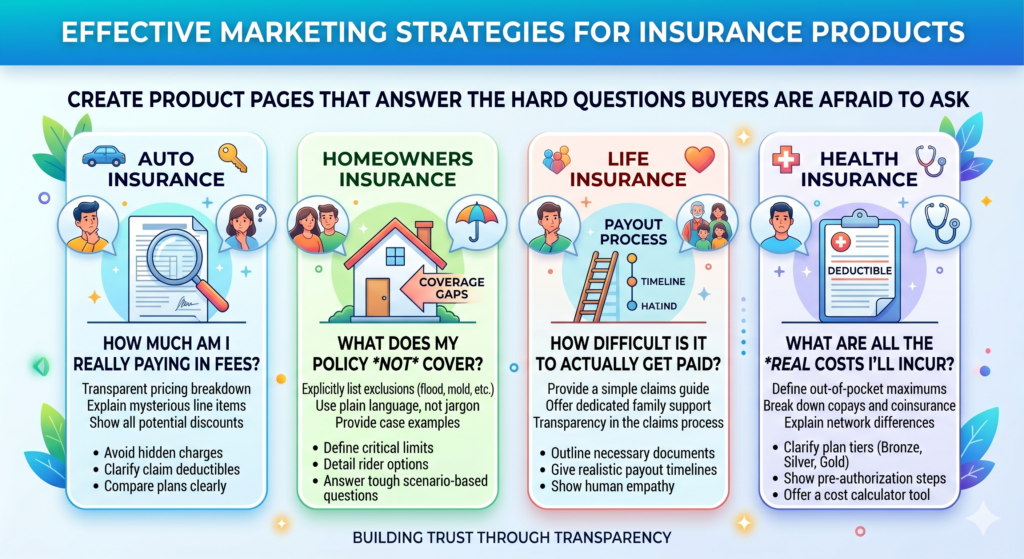

Create product pages that answer the hard questions buyers are afraid to ask

Most insurance product pages are too polite. They explain what the product is, add a form, and then hope the buyer takes action. But real buyers have harder questions in their minds. They want to know what is covered, what is not covered, why prices change, whether the policy is worth it, and what could go wrong if they choose the wrong plan.

If your product page avoids these questions, the buyer may go somewhere else to find the answers. Once that happens, you may lose control of the decision.

Strong product pages reduce hidden fear

Hidden fear is one of the biggest reasons insurance buyers delay action. They may not understand the policy. They may fear being trapped in the wrong plan. They may worry that the claim will be denied. They may feel embarrassed to ask basic questions.

Your page should make those questions feel normal.

A helpful product page does not talk down to the reader. It says, in a simple way, “Here is what this product does. Here is who needs it. Here is when it may not be enough. Here is what affects cost. Here is how to choose wisely.”

Explain what the product does not do

This is where many insurance pages become weak. They only talk about benefits. They avoid limits, exclusions, and cases where another type of cover may be needed.

That may feel safer from a sales point of view, but it can reduce trust. Buyers know every insurance product has limits. If your page does not mention them at all, the page may feel incomplete.

You do not need to turn the page into a legal document. You can simply explain that every policy has terms and exclusions, and that your team helps the customer review them before choosing. You can also explain common examples in plain words.

For example, a business liability page can say that general liability may help with certain third-party injury or property damage claims, but it may not cover professional mistakes, employee injuries, or damage to your own business property. Then you can guide the reader toward related cover options.

That kind of honesty creates confidence.

Price content should educate, not trap the buyer

Many insurance brands avoid talking about price because premiums depend on many factors. That is understandable. But avoiding price completely can frustrate buyers. People want at least a basic idea of what affects cost.

You do not always need to publish fixed prices. You can explain price factors, common cost drivers, and ways to compare value.

Show why the cheapest policy may cost more later

Insurance buyers often compare by price because price is easy to understand. Coverage quality is harder to judge. Your content should help them see the full picture.

A cheap plan may have a higher deductible, lower limits, fewer covered events, weaker support, or gaps that only become clear during a claim. Explain this without sounding pushy.

A simple way to say it is this. The best policy is not always the cheapest one. It is the one that gives enough protection for the risks the buyer truly faces, at a price they can afford.

This kind of message helps buyers make better choices. It also helps your brand attract people who value guidance, not just the lowest quote.

Add comparison sections that guide decisions

Insurance buyers compare options even if you do not help them do it. They compare providers, plans, coverage types, and prices. If your page does not guide that comparison, the buyer may rely on another website that does.

Comparison content can make your product page more useful and more persuasive.

Compare choices in plain language

If you sell life insurance, explain term life and permanent life in simple words. If you sell business insurance, explain general liability and professional liability. If you sell health insurance, explain network, deductible, copay, and out-of-pocket costs.

The goal is not to overwhelm the reader. The goal is to help them feel less lost.

A good comparison section should make the buyer think, “Now I understand which path may fit me.” Once the buyer feels that, they are more likely to take the next step.

Build content for every stage of the insurance buying journey

Insurance buyers do not move in a straight line. They may read a blog post, leave, return through a search ad, compare providers, ask a spouse or business partner, check reviews, and then request a quote days or weeks later.

A strong content strategy supports that full journey. It does not rely on one blog post or one landing page to do all the work.

Early-stage content should make the topic less confusing

At the start, buyers may not know what they need. They may only know they have a problem or risk. This is where simple educational content works well.

For example, a new business owner may search for what insurance is needed to start a business. A new parent may search for when to buy life insurance. A homeowner may search for what home insurance covers after hearing about damage in their area.

These people are not always ready to request a quote, but they are worth helping.

Teach without rushing the sale

Early-stage content should feel generous. It should explain the issue clearly and help the reader avoid mistakes. The call to action can be soft, such as inviting the reader to learn more, download a checklist, or speak with an advisor when ready.

This builds memory. When the person becomes ready, they are more likely to return to the brand that helped them first.

Good early-stage content also helps SEO because it answers the real questions people search before they buy.

Middle-stage content should help buyers compare

In the middle stage, people understand the product but are not sure which option is right. They may compare policy types, providers, price ranges, cover levels, or risks.

This is where content should become more practical.

A middle-stage article might explain how to choose the right liability limit, how to compare life insurance quotes, how to review a health insurance plan, or how to decide whether a small business needs added cover.

Help the buyer make a safer choice

Middle-stage buyers need decision support. They do not only need definitions. They need trade-offs.

For example, you can explain that a higher deductible may lower monthly cost, but it also means the customer pays more out of pocket if a claim happens. You can explain that lower premiums may look attractive, but the buyer should also review limits, exclusions, and service quality.

When you explain trade-offs, you sound more like an advisor and less like a seller.

Late-stage content should remove final friction

Late-stage buyers are close to action. They may search for reviews, quote pages, local agents, provider comparisons, or claim support details. They are looking for reasons to trust or reasons to walk away.

Your late-stage content should be direct, clear, and reassuring.

Make the next step feel low-risk

A late-stage page should explain what happens after the buyer contacts you. It should show that there is no pressure to choose immediately. It should make the form simple. It should include proof. It should answer final questions about timing, documents, support, and follow-up.

This is also where strong calls to action matter. But they should still feel human.

Instead of only saying “Submit,” use language that reflects the buyer’s goal. Say “Compare your options,” “Talk to an advisor,” or “Start your quote.” These feel more useful and less cold.

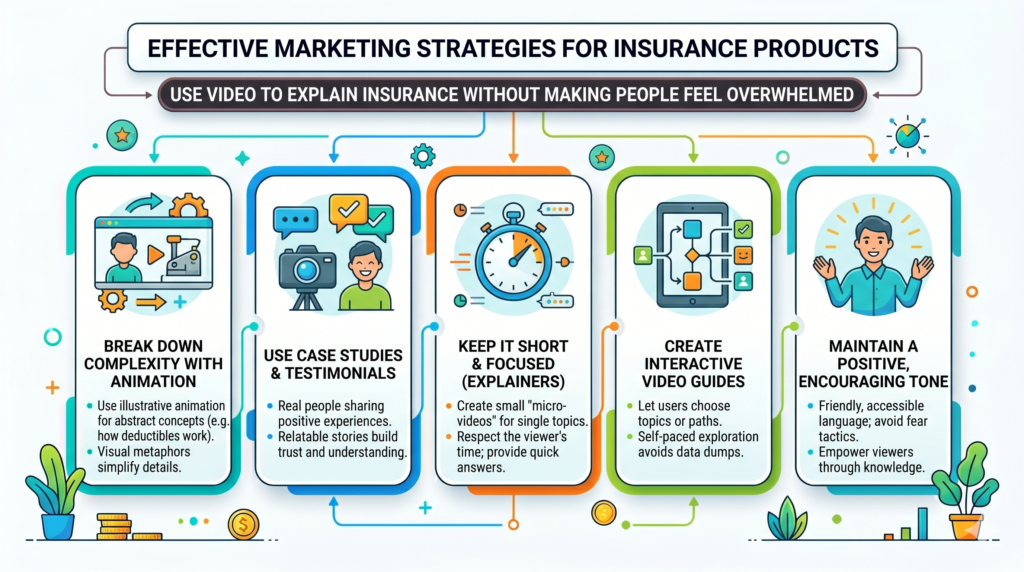

Use video to explain insurance without making people feel overwhelmed

Video can be very powerful for insurance because some topics are easier to understand when a real person explains them. A short video can turn a complex policy idea into a simple story. It can also make your brand feel more human.

But video should not be used just because it is popular. It should solve a clear communication problem.

Use video where trust and clarity matter most

Some insurance topics create more confusion than others. Deductibles, exclusions, policy limits, riders, waiting periods, claims, renewals, and business coverage types can all feel hard to understand.

A short video can explain these topics in a calm, simple way.

Keep each video focused on one question

The best insurance videos are not long lectures. They answer one question clearly. For example, “What is a deductible?” or “What does general liability insurance cover?” or “How much life insurance may a parent need?”

A focused video is easier to watch. It is also easier to reuse across your website, emails, social posts, and sales follow-ups.

The script should sound natural. Avoid reading policy language word for word. Use examples. Speak like a helpful advisor. End by telling the viewer what to do next if they want help.

Use customer stories carefully and respectfully

Customer stories can be powerful in insurance because they show real outcomes. But they must be handled with care. Insurance often deals with private, painful, or sensitive events.

A good story should focus on the problem, the support given, and the lesson learned. It should never expose private details without clear permission. It should never make a claim that could mislead future buyers.

Show the value of support, not just the product

Many brands use customer stories only to say the product was useful. A stronger story shows how the team helped the customer understand options, prepare documents, review cover, or handle a stressful moment.

This matters because insurance is not only the policy. It is also the support around the policy.

A buyer may forget the exact terms of a plan. But they will remember that your team helped someone during a hard time. That memory builds trust.

Use video in sales follow-up

Video does not have to be public to be useful. Short personal videos can help agents and advisors follow up with leads.

For example, after a quote request, an advisor can send a short video explaining what was reviewed, what the next step is, and what the customer should look at before deciding. This can feel more personal than a plain email.

Make follow-up feel more human

A short video can reduce the distance between the buyer and the advisor. It shows a face, a voice, and a real person behind the process.

This is especially useful for complex products like life insurance, business insurance, health insurance, or high-value home insurance. When the decision feels serious, human presence can increase confidence.

Video should not replace clear written information. It should support it. The buyer should still have the details in writing, but the video can make the message warmer and easier to understand.

Turn social media into a trust channel, not a vanity channel

Social media is not always the fastest direct sales channel for insurance. People may not buy a policy after one post. But social media can build familiarity, answer common questions, and make your team feel approachable.

The problem is that many insurance brands post content that feels too generic. They share holiday greetings, stock images, and broad protection quotes. This may keep the page active, but it does not build strong demand.

Social content should teach small, useful lessons

A good social post should help the audience understand one small thing about risk, cover, claims, cost, or planning. It should be simple enough to read quickly and useful enough to remember.

For example, a post can explain why a renter may still need insurance even if the landlord has a policy. Another can explain why a growing business should review coverage after hiring employees. Another can explain why adding a teen driver may affect auto insurance costs.

Use real questions from customers

Your best social content often comes from questions your customers already ask. If one person asks a question, many others may have the same concern.

Turn these questions into posts, short videos, reels, carousels, or simple explainers. Keep the language natural. Do not make the post sound like a compliance document. If a topic needs a disclaimer, include it clearly, but still explain the core idea in plain words.

This approach makes social media easier to manage because you are not inventing random content ideas. You are answering real questions.

Build authority by being consistently helpful

Insurance buyers may not engage with every post. They may not comment or share. But they notice patterns. If your brand keeps showing up with useful, simple, honest advice, people start to remember you.

That memory matters when a need appears.

Do not chase trends that do not fit the product

Not every trend fits insurance. A funny trend may get attention, but if it makes the brand look careless, it can hurt trust. Insurance deals with serious risks. The tone can be warm and human, but it should not become careless.

This does not mean social content must be boring. It can be friendly, clear, and relatable. But the message should still support the brand promise.

A good test is simple. After seeing your post, would a buyer feel more confident asking you about insurance? If the answer is yes, the content is useful. If the answer is no, the content may only be noise.

Use social proof in a natural way

Reviews, customer feedback, community work, team stories, and behind-the-scenes content can all help build trust. But they should not feel forced.

Show real moments. Show your team explaining something. Show how you help customers prepare for renewals. Show local involvement. Show education sessions. Show common mistakes people can avoid.

Make the brand feel reachable

Insurance can feel cold when it is only shown through forms and policy terms. Social media gives you a chance to show people that there are humans behind the brand.

This matters because people often want to ask questions before they buy. If your social presence feels helpful and reachable, they may be more willing to send a message, book a call, or visit your website.

Social media may not close every sale directly. But it can warm the market, support retargeting, improve trust, and make every other channel work better.

Build referral marketing into the customer experience

Referral marketing works well for insurance because trust is already hard to earn. When a friend, family member, client, accountant, real estate agent, lender, lawyer, or business partner recommends you, the buyer starts with less doubt.

But referrals do not happen only because customers like you. They happen when customers remember you, understand who you help, and feel safe putting their name behind the recommendation.

A referral system should feel natural, not forced

Many insurance brands ask for referrals in a rushed way. They send one email saying, “Refer a friend,” and then stop. That rarely works well because the customer may not know who to refer, why to refer, or when to refer.

A better referral strategy is built into the customer journey. You ask after moments of value. You make it easy to share. You explain the type of people you can help. You thank the customer properly.

Ask after you have helped the customer

The best time to ask for a referral is after a customer has experienced clear value. This could be after you helped them compare options, explained a confusing policy, supported them during renewal, solved a claim-related concern, or helped them save time.

At that moment, the customer is more likely to remember the value of your service.

The request should be simple and warm. You can say that many of your best customers come from people who already trust your team. Then explain that if they know someone who needs help understanding their insurance options, you would be happy to guide them.

That feels better than asking, “Do you know anyone who wants to buy insurance?” The first version is about help. The second version is about selling.

Partner referrals can create a strong growth channel

Insurance often connects with other life and business events. People need insurance when they buy homes, start businesses, hire employees, take loans, lease offices, buy cars, sign contracts, travel, get married, have children, or plan estates.

This creates natural partner opportunities.

Real estate agents can refer home insurance buyers. Mortgage brokers can introduce homeowners. Accountants can refer business owners. Lawyers can refer clients who need risk planning. HR consultants can refer companies reviewing employee benefits. Car dealers can refer auto insurance leads.

Build partner value before asking for leads

A referral partner should not feel like a lead source you are trying to use. They should feel like a professional relationship where both sides help the client.

If you want stronger partner referrals, give partners tools that make their work easier. Share simple guides they can give clients. Offer quick insurance checklists. Help them understand when a client may need coverage. Make the handoff easy and professional.

For example, a real estate agent does not want their buyer delayed because insurance paperwork becomes confusing. If you make that process smoother, you become useful to the agent. That usefulness can turn into repeat referrals.

Make the referral path easy to follow

Even happy customers and partners may not refer if the process feels unclear. They should know exactly what to do.

Should they share a link? Send an email intro? Give the person your phone number? Fill out a form? Ask the person to book a call? The easier the path, the more likely the referral happens.

Give people simple words they can use

Most customers do not know how to explain your value clearly. Help them.

You can give them a short message they can forward. It should sound human and not scripted. For example, it can say that they worked with your team and found the process clear and helpful, and that your team may be able to help compare insurance options.

This removes effort from the customer. It also helps the referred buyer understand why they are being introduced.

Referral marketing is not just a campaign. It is a trust system. When you serve people well, make your value easy to remember, and create simple ways to introduce others, referrals can become one of the most profitable channels in insurance.

Use customer retention as a marketing strategy, not just a service task

Insurance marketing should not end after the policy is sold. In many cases, the real profit comes from retention, renewals, cross-sells, upsells, and long-term relationships.

A customer who stays for years is more valuable than a lead who buys once and leaves. A customer who trusts you may buy more products over time. They may also refer others. This is why retention is not only a service issue. It is a marketing strategy.

Keep helping after the sale

Many insurance companies become quiet after the customer buys. The customer hears from them only when a payment is due, a renewal is coming, or a problem happens. That creates a weak relationship.

If the customer only sees you as a bill, they may switch when someone offers a lower price. If they see you as a helpful advisor, they are more likely to stay.

Create simple check-in moments

A good retention strategy includes planned check-ins during the year. These do not need to be long or complex. They should simply help the customer review whether anything has changed.

For a family, changes may include a new home, new child, new car, new job, or new driver. For a business, changes may include more staff, new equipment, new locations, larger contracts, new services, or higher revenue.

These moments matter because insurance needs can change quietly. If you help customers notice these changes, you protect them better. You also create natural chances to update coverage.

Make renewals feel like reviews, not invoices

Renewal is one of the most important marketing moments in insurance. It is when the customer decides whether to stay, shop around, reduce coverage, or move to another provider.

Too many brands treat renewal like a transaction. They send a notice, state the price, and wait. That is not enough.

Explain what changed and what the customer should review

A strong renewal message helps the customer understand what they are renewing. It explains key details in simple words. It invites them to review coverage before making a decision. It also gives them a chance to ask questions.

If the premium changed, explain common reasons prices may change, without making promises or giving unsupported claims. If coverage options changed, explain what the customer should look at. If their life or business has changed, encourage them to update their details.

This makes renewal feel like care. It also reduces the chance that the customer shops only on price.

Cross-sell only when it is truly useful

Cross-selling can grow revenue, but it must be done carefully in insurance. If the offer feels random, it can reduce trust. If it is tied to a real customer need, it can feel helpful.

For example, a home insurance customer may also need auto insurance, umbrella coverage, or life insurance. A small business owner may need general liability, commercial property, workers’ compensation, professional liability, or cyber coverage depending on their work.

Connect the offer to a real risk

Do not say, “You may also like this policy.” That sounds like eCommerce. Insurance cross-selling should explain why the added cover may matter.

If a customer has a growing business, explain that new contracts, staff, or equipment may create new risks. If a family buys a home, explain that it may be a good time to review life insurance because the mortgage creates a long-term responsibility.

The offer should feel like guidance. The customer should think, “That makes sense for my situation,” not “They are trying to sell me more.”

Retention grows when customers feel seen after the sale. If you keep helping, teaching, reviewing, and guiding, you create a relationship competitors cannot easily break with a cheaper quote.

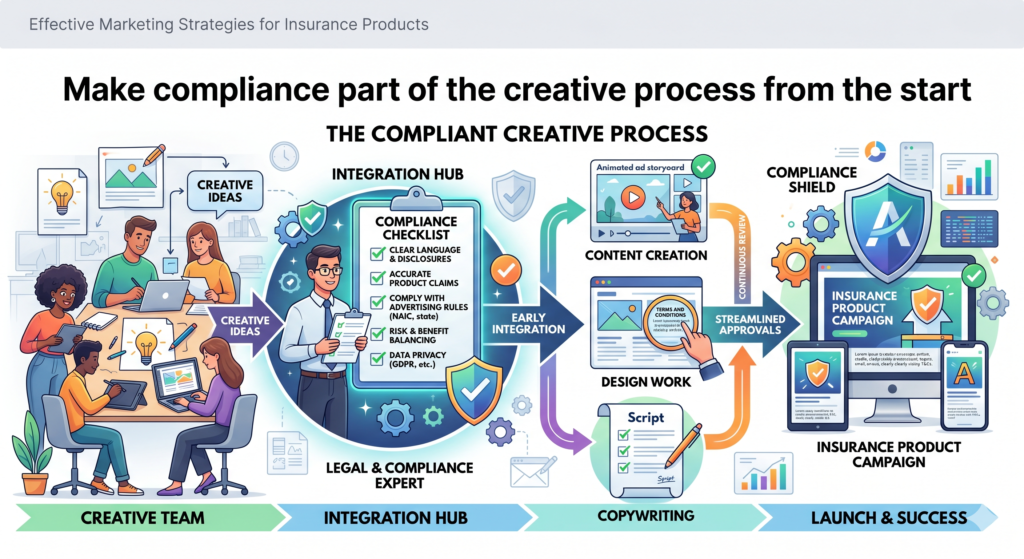

Make compliance part of the creative process from the start

Insurance marketing must be persuasive, but it must also be careful. This is not a space where marketers can make loose claims, hide key details, or use pressure tactics without risk.

Compliance should not be treated as the final step after the campaign is written. It should be part of the strategy from the beginning. This saves time, protects the brand, and builds more honest marketing.

Clear marketing is safer marketing

Many compliance problems begin with unclear language. A headline may sound exciting but imply too much. A claim may be true in some cases but not in all. A promise may depend on policy terms that are not explained nearby.

The safest path is often also the strongest path. Say what you mean. Avoid hype. Explain limits. Use plain language. Do not make the buyer guess.

Avoid claims that sound absolute

Insurance products usually depend on terms, conditions, eligibility, exclusions, limits, location, and underwriting. So absolute phrases can be risky.

Phrases like “full protection,” “guaranteed savings,” “complete coverage,” or “claim approval assured” can create problems if they are not strictly true. They may also make careful buyers skeptical.

A better approach is to use grounded language. Say that a policy may help protect against certain risks. Say that your team can help compare suitable options. Say that coverage depends on the terms of the policy.

This may sound less flashy, but it builds more trust. In insurance, trust usually sells better than hype.

Involve compliance before production

Many teams create ads, pages, emails, videos, and brochures first, then send them for approval at the end. This often leads to delays and rewrites.

A smarter workflow is to involve compliance early. Before writing the full campaign, agree on the allowed claims, required disclaimers, product limits, approved proof points, and words to avoid.

Create reusable approved language

Insurance brands can save time by building a library of approved wording. This can include product descriptions, disclaimer lines, claim explanations, pricing language, coverage limit explanations, and compliant calls to action.

When writers and marketers have approved language, they can move faster without starting from scratch each time.

This does not mean every page should sound the same. The approved language is the safe base. The copywriter can still make the page clear, human, and engaging around it.

Make disclosures easy to understand

Disclosures are important, but they should not feel hidden. If important details are buried in tiny text, buyers may feel misled. Even if the wording is technically present, the experience can damage trust.

Good marketing makes important limits visible and understandable.

Explain the meaning behind the disclaimer

When a disclaimer is needed, add simple context near it where possible. For example, if coverage depends on policy terms, explain that the customer should review what is covered and not covered before choosing. If availability varies by location, say that options may differ depending on where the customer lives or operates.

This helps the buyer understand the message. It also supports a better customer experience.

Compliance does not have to weaken copy. Done well, it can make copy clearer, stronger, and more trustworthy. That is exactly what insurance marketing needs.

Use data to improve campaigns without losing the human touch

Insurance marketing should be measured carefully. But numbers alone do not tell the full story. A campaign may bring cheap leads that never buy. Another may bring fewer leads but better customers. A blog post may not convert directly, but it may help future buyers trust your brand.

The goal is to use data to make better decisions, not to chase the easiest numbers.

Track the full journey, not just the first click

Many insurance marketers look only at traffic, cost per click, form fills, or call volume. These numbers matter, but they are not enough.

You also need to know which leads become qualified, which quotes become policies, which customers renew, and which channels bring long-term value.

Measure lead quality by source

A lead from a broad social campaign may behave differently from a lead from a high-intent search ad. A lead from an educational blog post may need more nurturing. A referral lead may close faster because trust is already present.

If you measure all leads the same way, you may invest in the wrong channels.

Track where each lead came from, what they asked for, how long they took to close, what product they bought, and whether they stayed. This helps you see which marketing channels are truly profitable.

Use call tracking and CRM notes wisely

Insurance leads often convert through calls, not only online forms. If you do not track calls properly, you may undercount the value of SEO, local pages, paid ads, emails, and referral campaigns.

Call tracking can show which campaigns generate phone leads. CRM notes can show what those leads cared about.

Turn sales conversations into content ideas

Your sales or advisory team hears buyer questions every day. These questions are gold for marketing.

If many callers ask why their quote is higher than expected, create content explaining price factors. If many business owners ask about certificates of insurance, create a guide. If many parents ask how much life insurance they need, create a simple planning article.

This creates a feedback loop. Marketing brings leads. Sales learns from leads. Those lessons improve marketing.

Test one major idea at a time

Marketing teams often change too many things at once. They change the headline, form, offer, image, audience, and landing page together. Then they cannot tell what worked.

A better approach is to test one major idea at a time.

Test messages before redesigning everything

Before rebuilding a full website or campaign, test different messages. Try a trust-focused headline against a savings-focused headline. Try a family protection angle against a price comparison angle. Try a short form against a guided form.

These tests can show what buyers care about most.

But do not let testing remove the human touch. Insurance is emotional. Data can show what people clicked. It cannot always explain why they hesitated, what they feared, or what finally made them trust you. That is why the best insurance marketing uses both numbers and empathy.

Build a brand voice that feels calm, clear, and dependable

Insurance brands often sound either too stiff or too sales-driven. One feels cold. The other feels pushy. The best voice sits in the middle. It is calm, clear, helpful, and dependable.

This matters because voice shapes trust. A buyer may not remember every sentence on your site, but they will remember how your brand made them feel.

Speak like a steady guide

Insurance decisions can feel heavy. People are thinking about accidents, illness, damage, loss, lawsuits, death, family needs, business risk, or money stress. Your brand voice should not add more pressure.

It should make the buyer feel that the next step is manageable.

Use simple words for serious topics

Simple words are not childish. They are respectful. They help people make better decisions.

Instead of saying “risk mitigation solutions,” say “ways to reduce financial risk.” Instead of saying “policyholder obligations,” say “what you need to do for the policy to work as expected.” Instead of saying “benefit eligibility,” say “who can use this benefit.”

This kind of language makes your brand easier to trust.

Do not scare people into buying

Fear is part of insurance, but fear-based marketing can go too far. If your message makes people panic, they may shut down or distrust you.

A better approach is to name the risk clearly, then show a calm path forward.

Balance risk with control

For example, instead of saying, “One mistake could destroy your business,” say, “One claim can be costly, but the right cover can help your business handle certain risks with more confidence.”

The second version still explains the risk. But it does not feel like a threat. It gives the reader a sense of control.

This is important because people act more easily when they feel guided, not frightened.

Keep the voice consistent across channels

Your brand should not sound warm on the website, aggressive in ads, stiff in emails, and cold during renewal. That creates confusion.

A clear voice should run through every touchpoint. Ads, landing pages, quote forms, emails, call scripts, renewal messages, social posts, and claim support content should all feel like they come from the same trusted team.

Write for the person, not the product

Before writing any message, ask what the buyer is feeling at that moment. Are they confused? Worried? Busy? Comparing? Skeptical? Ready to act?

Then write to that state.

A person filling out a quote form needs reassurance. A person reading a beginner guide needs clarity. A person opening a renewal email needs confidence. A person comparing policies needs help making a smart choice.

When your voice matches the buyer’s moment, your marketing feels more human.

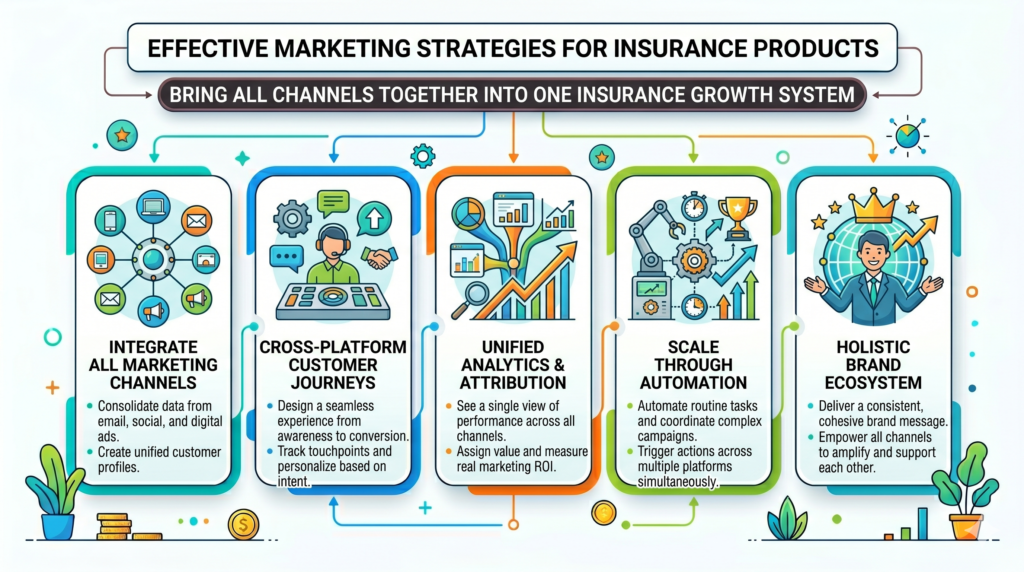

Bring all channels together into one insurance growth system

The strongest insurance marketing does not depend on one channel. SEO alone is too slow. Paid ads alone can become expensive. Referrals alone are not always predictable. Social media alone may not drive enough direct demand. Email alone needs leads to nurture.

The real power comes when all channels support each other.

Each channel should have a clear role

SEO captures people who are searching. Paid ads help capture demand and test messages. Social media builds familiarity. Email nurtures leads and supports retention. Local marketing builds trust. Referrals bring warm introductions. Product pages convert interest into action.

When every channel has a role, your strategy becomes easier to manage.

Stop judging every channel by the same metric

A blog post may not produce quote requests on the first visit, but it may bring a buyer into your world. A retargeting ad may not create new demand, but it may bring back someone who was already interested. A referral partner may not send high volume, but the leads may close at a higher rate.

Each channel should be judged based on its job.

This prevents short-term thinking. It also helps you avoid cutting channels that support the full buyer journey.

Build journeys, not random campaigns

A random campaign says, “Let us run ads for life insurance this month.” A journey says, “Let us help new parents understand their need, compare options, request guidance, and review coverage as their family grows.”

That difference matters.

Start with one product and one audience

You do not need to build a full marketing machine for every product at once. Start with one important product and one clear audience.

For example, focus on life insurance for young families, business insurance for contractors, auto insurance for first-time drivers, or home insurance for new buyers. Build the full journey for that group. Create the SEO content, landing page, lead magnet, email sequence, ads, retargeting, referral message, and sales follow-up process.

Once that journey works, improve it. Then build the next one.

Keep improving the system every month

Insurance marketing is not something you set once and forget. Buyer questions change. Competitors change. Costs change. Search behavior changes. Regulations may change. Your strongest campaigns will come from steady improvement.

Review both performance and customer feedback

Each month, look at what the numbers say and what customers are saying. Which pages bring leads? Which ads bring qualified calls? Which emails get replies? Which questions keep coming up? Which objections slow down sales? Which customers renew? Which ones leave?

Use those answers to improve your content, forms, calls to action, follow-up, and product education.

This is how insurance marketing becomes a growth system. It gets smarter over time. It becomes more trusted. It wastes less money. It creates better leads. It helps buyers make better decisions.

Use claim support content to build trust before a claim ever happens

A big part of insurance trust is built around one question the buyer may not say out loud. “Will this company help me when I actually need them?”

Most insurance marketing talks about buying the policy. Very little talks about what happens after something goes wrong. That is a missed chance. Claim support content can make your brand feel more reliable because it shows buyers that you are thinking beyond the sale.

Buyers want to know the process before they need it

People often fear the claim process because they do not know what to expect. They worry about paperwork, delays, denied claims, unclear steps, and not knowing who to call. This fear can affect their buying decision even before they choose a policy.

Your marketing can reduce this fear by explaining the claim process in simple words.

Do not wait until someone has a claim to explain how claims work. Add claim support content to your website, emails, welcome materials, product pages, and customer portal. Make it easy to find. Make it calm. Make it useful.

Explain the first step clearly

The first step after a loss is often the most stressful. A customer may be upset, confused, or worried about money. Your content should tell them what to do first, who to contact, what information to collect, and what they should avoid doing before speaking with the right person.

For example, a home insurance customer may need to document damage, take photos, protect the property from further damage when safe, and contact the claims team. A business insurance customer may need to record details of the incident, save documents, and notify the insurer quickly.

This kind of guidance creates comfort. It tells buyers that your team understands the real-life stress behind insurance.

Claim content should be honest about limits

This is important. Claim support content should never promise that every claim will be paid. It should never make the process sound simpler than it is. That can create trust issues later.

Instead, explain that claims are reviewed based on the policy terms, documents, coverage, exclusions, and facts of the situation. Then explain how your team helps the customer understand the process.

This is honest and still reassuring.

Show customers how to prepare before a problem happens

Some of the best claim content is preventive. It teaches customers how to stay ready.

For home insurance, you can create content on keeping records of valuable items, reviewing coverage after renovations, and understanding deductibles. For business insurance, you can explain the value of keeping contracts, invoices, safety records, and incident reports.

For auto insurance, you can explain what details to collect after an accident.

This content helps customers before there is a crisis. It also lowers confusion if a claim happens later.

Claim support content can also help sales teams

Sales teams and advisors often answer claim-related questions during the buying process. If you create strong claim support pages, they can use them in follow-up emails and calls.

This makes the sales process smoother. Instead of giving a rushed verbal answer, the advisor can share a clear page that explains the process.

Turn claim questions into trust assets

Every claim-related question is a chance to create content. If customers often ask how long claims take, create a page explaining the factors that can affect timing. If they ask what documents are needed, create a checklist-style page written in paragraph form. If they ask why claims may be denied, create a careful educational article explaining common reasons.

This kind of content is not just customer service. It is marketing. It gives buyers proof that your brand is useful when things are hard.

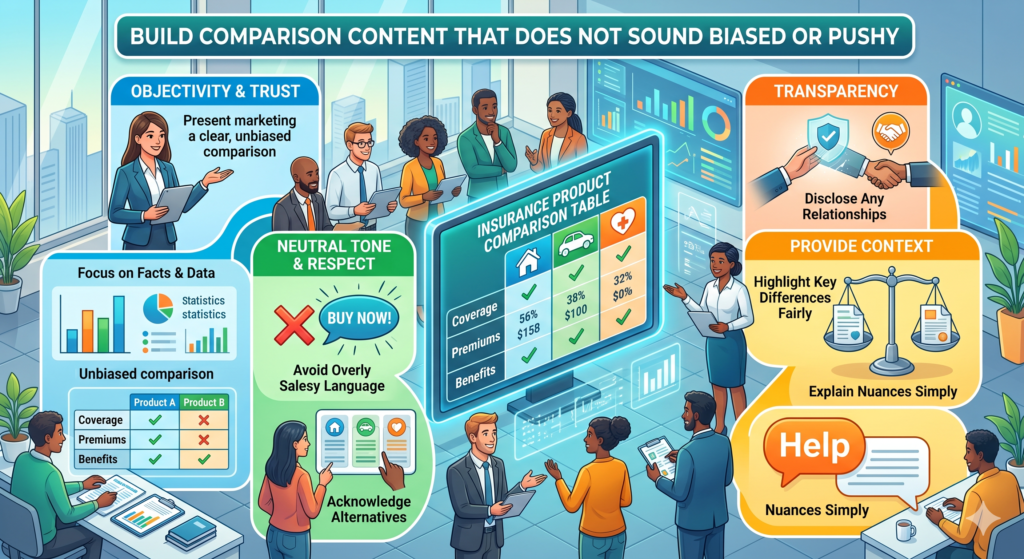

Build comparison content that does not sound biased or pushy

Insurance buyers compare everything. They compare companies, policy types, price levels, coverage limits, add-ons, deductibles, and customer reviews. If you do not help them compare, another website will.

Comparison content is powerful because it meets buyers at a high-intent stage. These people are not just casually learning. They are trying to make a choice.

Honest comparison builds more trust than one-sided selling

Many brands are afraid to compare options because they do not want to mention alternatives. But buyers already know alternatives exist. If your content pretends there is only one good answer, it may feel less credible.

A better approach is to explain who each option may suit and where each option may fall short.

For example, when comparing term life insurance and permanent life insurance, do not say one is always better. Explain that term life may be useful for people who want cover for a set period, such as while raising children or paying a mortgage.

Permanent life may suit people who want lifelong cover and are comfortable with higher premiums, depending on their goals and eligibility.

Use “best fit” language instead of “best overall” language

Insurance choices depend on the buyer. That is why “best” can be risky and unclear. A product may be best for one person and wrong for another.

Use language like “may fit,” “can be useful when,” “often suits,” and “worth reviewing if.” This sounds more honest. It also helps the buyer think about their own situation.

The goal is not to force a decision. The goal is to help the buyer make a better decision. That is what makes comparison content persuasive.

Compare based on real decision factors

Weak comparison pages compare shallow details. Strong comparison pages compare what actually affects the buyer’s choice.

For insurance, decision factors often include price, coverage limits, exclusions, claim support, policy flexibility, customer service, eligibility, renewal terms, waiting periods, deductibles, add-ons, and support during purchase.

Each factor should be explained in plain words.

Explain trade-offs clearly

A lower premium may be helpful for monthly budget, but it may come with higher out-of-pocket costs or lower limits. A higher coverage limit may cost more, but it may offer more protection for larger risks. A simple policy may be easier to manage, but it may not cover more complex needs.

Trade-offs help buyers understand that insurance is not only about price. It is about fit.

When you explain trade-offs well, you also reduce poor-fit leads. People who only want the cheapest option may self-select out. People who value guidance may move closer to your team.

Use comparison content across channels

A good comparison article should not live only on your blog. It can support paid ads, email nurture, retargeting, sales follow-up, and social content.

For example, if someone visits a product page but does not request a quote, you can retarget them with a comparison guide. If a lead asks about price, you can email them a page explaining how to compare value. If a salesperson keeps hearing the same objection, comparison content can help answer it at scale.

Keep comparison pages updated

Insurance products, pricing, customer needs, and regulations can change. Comparison content must be reviewed often. An outdated comparison page can hurt trust and create risk.

Set a review schedule for your most important comparison pages. Check whether the advice is still accurate. Check whether product names, coverage details, market conditions, and calls to action still make sense.

Fresh comparison content can become a long-term growth asset. It helps SEO, supports sales, and gives buyers confidence at one of the most important points in the journey.

Conclusion

Effective marketing for insurance products is not about pushing people into quick decisions. It is about helping them feel safe, clear, and ready to act.

Insurance buyers are often careful because the product feels serious. They want to know what is covered, what is not covered, what it may cost, and whether they can trust the people behind the policy. Your marketing must answer those questions before doubt grows.

Comments are closed.